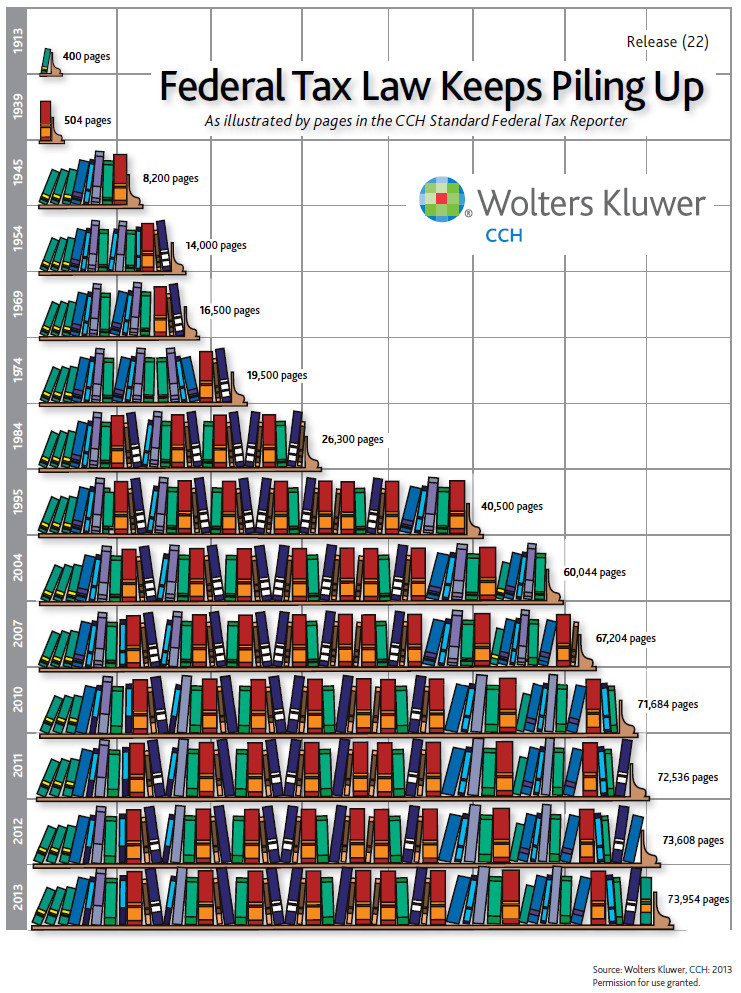

ANTONIO ROMANO — “The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several states, and without regard to any census or enumeration.” In 1913 the states ratified the 16th Amendment, and in doing so gave birth to the Federal Income Tax. At its advent, the United States Income Tax Code was approximately 400 pages. Today, the tax code is 73,954 pages. What was once shorter than most law books is now a series of codes and exceptions, exceptions to exceptions, outdated logic, and cross references that lead no where. There have been calls for revision and updating, though no one has yet to take on the daunting task of overhauling the tax system. Instead, the code continues to become more complicated, and the 955 page Compilation of Patient Protection and Affordable Care Act has not helped.

Enacted in early 2010, the Affordable Care Act was set to reform both the public and private health insurance systems, with intent on making healthcare coverage affordable and accessible to every American. Though some provisions took effect early on, major provisions are expected to take effect in January 2014. But where is the funding for the provisions coming from? From taxes and penalties on both healthcare and non-healthcare related items and services.

Most of the taxes are aimed at higher net worth individuals and private insurance providers, but the rates are not indexed for inflation so the threshold amounts ensnare more individuals each year. For example, individuals that report $200,000 or joint filers that report $250,000 can expect increases such as a .9% Increase in Medicare Tax Rate, a 3.8% New Tax on unearned income, and a 3.8% New Tax on investment income.

Most of the penalties are aimed at businesses and individuals who do not become insured. One provision of the Act is that a business with fewer than 50 full-time employees is not required to provide coverage and a business with fewer that 25 full-time employees may receive a tax credit to offset the costs of providing coverage. What effects will that have on business hiring decisions? Will a small business owner lay off employees to fall beneath the threshold and receive the credits, or simply deny coverage altogether to avoid the hassle of the new system? Workers who do not put in more than 30 hours per week will not be required to be covered. Businesses could also use that to their advantage and cut employee hours to fall beneath the thresholds. While there is anecdotal evidence of the above things happening, there is no evidence that those cases have added up to a broader drag on the economy as a whole. But the coverage has yet to take full effect, and only time will tell what will happen in the future.

Businesses with over 50 full-time employees are required to provide coverage to their employees. Come 2015, businesses will be required to report whether insurance has been provided and what type. If a business does not provide insurance, it will be assessed a penalty of $2,000 for every employee in the company if even one employee opts to obtain insurance through an exchange. However, the first 30 employees are not counted in calculation of the penalty. So an employer with 75 employees would pay the penalty for 45 workers, or $90,000 (45 x $2.000). There is also a penalty for providing insurance that is “too expensive.” Employers with more than 50 employees that do provide insurance must pay a penalty if any of their employees obtain a subsidy to help pay for insurance. The penalty equals $3,000 per worker who uses the subsidy or $750 for every employee at the company, whichever is less.

The above is merely a drop in the ocean that is the Compilation of Patient Protection and Affordable Care Act. Confusing? Immensely. But the failure to provide coverage and pay attention to the rules could result in losing out on credits, or worse, owing money to the IRS in the future.

Anxious to draw upon the momentum of the implementation of nationwide healthcare coverage, what has been spawned is an act that those who passed it do not fully understand, a government shut-down in an attempt to halt its implementation, a Supreme Court decision, and a website that does not work. Rife with increases, exceptions, credits, and penalties, the Act is likely to spawn a whole area of consulting and issues related to the implementation and providing of coverage to employees of companies. Though the concept of no American being denied the right to affordable healthcare is a noble one, the expediency with which the Act was passed has led to a half-cocked system that may not survive the 2016 office. Though, as of now, only time will tell.

{kind=link}